The Hidden Benefits of Escrow Account Interest

Escrow accounts are a necessity for homeowners as they handle the tax and insurance payments. And with tech, they’re changing. Blockchain-based escrow models are growing rapidly, with an expected market value of $11.5 billion by 2033 (Source).

But can the funds in there earn escrow account interest rate. It really depends on how big of an amount is parked there.

And all of this must be managed competently as the tax and insurance payments also have to be paid on time.

In this article, I’ll tell you everything about Escrow accounts and the interest earning capability they possess. The following sections discuss their limitations, how interest earning impact liquidity, how to manage tax and insurance while doing that, etc.

KEY TAKEAWAYS

- Escrow funds can earn you interest but it can impact your liquidity.

- There are many structural limitations to escrow accoutns, and managing many across LLCs is quite challenging.

- You have to report all escrow account activity indluign interest to IRS.

- Start seeing it as a component in your financial system.

How Escrow Interest Impacts Portfolio Liquidity

Nobody even thinks of touching the reserved balance but those accounts hold significant capital of yours as property taxes and insurance accumulate over years. At scale, this results in:

- Idle capital that is not integrated into portfolio-level cash flow planning

- Reduced visibility into available liquidity during acquisition or CapEx cycles

- Fragmented tracking across entities, especially when lenders operate on separate systems

The hidden benefit is not just the interest earned. It is the opportunity to reframe escrow as part of your broader liquidity model. At your portfolio size, liquidity is not just about access. It is about timing. Trust accounts introduce structured outflows that are predictable. When those flows are mapped correctly, they can improve how you allocate reserves across entities. This becomes especially relevant when you are balancing:

- Quarterly estimated taxes tied to rental income

- Insurance renewals across staggered policy timelines

- Local property tax cycles that vary by jurisdiction

Interest on escrowed funds, even at modest levels, signals that these balances are active financial components. Not static obligations.

The Structural Limitations of Traditional Escrow Systems

Escrow framework has been quite simple. Traditional banks and lending institutions typically manage reserves at the loan level, while platforms like Baselane provide the necessary visibility at the portfolio level. This works for a small number of properties. It becomes operationally complex when applied across a multi-entity portfolio. Common constraints include:

- Lack of consolidated reporting across escrow accounts

- Limited transparency into how interest is calculated or applied

- Disconnected data from your primary operating accounts

At scale, these limitations create friction in three areas. First, reconciliation. Trust inflows and outflows often require manual tracking to align with bookkeeping systems. This increases the risk of misclassification when preparing Schedule E.

Second, forecasting. Without centralized visibility, projecting future obligations across multiple LLCs becomes less precise. Third, audit readiness. Inconsistent reporting across lenders can complicate documentation during tax preparation or financial reviews. These systems are not flawed.

The Role of Escrow Interest in Yield Optimization

But why would you even look at earning interest on escrowed funds when there are other more attractive instruments already available? Still, the presence of interest introduces a baseline expectation. Capital held in reserves should not be entirely non-productive. At scale, even a marginal yield contributes to portfolio efficiency. According to the Federal Reserve’s data on deposit account returns, interest-bearing accounts have historically provided modest but consistent returns relative to non-interest-bearing structures.

While escrow accounts are not fully comparable to standard deposit accounts, the principle still applies. Idle funds have an opportunity cost. For investors managing 10 or more units, this cost becomes measurable. Consider a portfolio where trust balances across properties total six figures over the course of a year. Even a small percentage yield offsets operational costs. More importantly, it reinforces disciplined tracking of these balances. The hidden advantage is behavioral. When escrow accounts generate interest, they are more likely to be monitored, reconciled, and integrated into financial planning. That reduces the risk of:

- Overfunding reserves beyond required thresholds

- Missing discrepancies in lender calculations

- Overlooking timing mismatches between reserve disbursements and actual expenses

Escrow interest creates a feedback loop. It encourages attention.

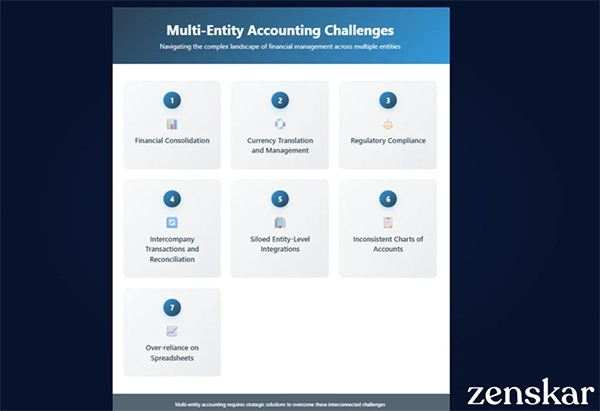

Multi-Entity Complexity and Escrow Fragmentation

Coordinating trust funds across multiple LLCs becomes quite a challenge. Each entity may have:

- Different lenders with unique escrow policies

- Separate tax jurisdictions with varying payment schedules

- Distinct insurance providers and renewal timelines

The following infographic lists all the challenges associated with managing multi-entity accounts, be it reserves or otherwise:

This fragmentation introduces operational overhead. At your portfolio size, the challenge is not understanding escrow. It is managing it efficiently across entities. Key friction points include the following:

- Tracking trust balances alongside operating cash without duplication

- Aligning escrow disbursements with expense recognition for tax reporting

- Maintaining clean separation between entities while still achieving portfolio-level visibility

Most generic accounting software is not designed for this stage of granularity. It may track transactions, but it regularly requires manual structuring to mirror escrow as it should be. Property control structures awareness on rent collection and tenant workflows. Escrow sits outside their core architecture.

This leaves a gap. Some investors are using platforms to centralize rental banking and bookkeeping across multiple LLCs. This can make it easier to align trust flows with operating accounts and Schedule E reporting. The value is not in replacing escrow. It is in integrating its data into a unified financial view.

Escrow Interest and Tax Reporting Alignment

Escrow activity, including earning interest, has to be reported to the IRS in terms of account and owner details.

At scale, the challenge is consistency. Across multiple lenders, interest reporting may vary. A few institutions issue 1099-INT forms. Others may not, depending on thresholds or account structure. For investors managing several LLCs, this creates risk in two areas:

- Incomplete reporting of interest income

- Misalignment between escrow disbursements and deductible costs

Schedule E requires accurate tracking of costs be it property taxes or insurance. If trust disbursements aren’t simply mapped, it could lead to timing discrepancies. For example:

- Taxes paid from escrow may not align with when the expense is recorded

- Insurance premiums may be recognized differently across entities

Reserve interest adds another layer. Even if the amounts are small, they must be accounted for consistently. This reinforces the need for systems that connect escrow activity with entity-level bookkeeping. The hidden benefit here is discipline. Interest on escrowed funds forces a closer alignment between lender activity and your internal records.

Operational Efficiency Through Escrow Visibility

Managing any opaque account like a trust fund is as good as shooting an arrow in the dark. Visibility enables control. When they are integrated into your financial system, they become predictable components of your operations. At scale, this shift has measurable effects. Improved visibility enables the following:

- More accurate cash flow forecasting across entities

- Faster reconciliation during monthly closes

- Reduced time spent preparing tax documentation

It also supports better decisions. When you understand how much capital is tied up in escrow at any given time, you can make More informed choices.

- Refinancing strategies

- Reserve allocation across properties

- Timing of large expenditures

Escrow interest, while small in isolation, acts as a signal. It indicates that these balances are active and should be tracked accordingly.

Reframing Escrow as a Financial System Component

Most investors treat reserves almost as a liability. But you’ve to see it a component of your financial system. It sits between your operating cash and your long-term obligations. This layer has defined characteristics:

- Predictable inflows based on lender requirements

- Scheduled outflows tied to taxes and insurance

- Limited but measurable yield through interest

When incorporated into your financial system, escrow can enhance the following:

- Planning accuracy

- Reporting consistency

- Capital efficiency

- The shift is conceptual.

Instead of isolating trust funds, you integrate them. This requires:

- Centralized tracking across all entities

- Consistent categorization within your bookkeeping system

- Clear mapping between escrow activity and tax reporting

The benefit is not just clarity. It is control.

Escrow Strategy as a Signal for Portfolio Maturity

Escrow is a good signal of your portfolio maturity. Investors who actively track trust balances, interest accrual, and disbursement timing tend to operate with tighter financial systems. This is not about optimizing yield. It is about reducing uncertainty across multiple LLCs.

When escrow is treated as part of your financial infrastructure, it reveals how well your portfolio is aligned. Gaps become visible faster. Discrepancies surface earlier. Reporting becomes more consistent. This level of management matters when you are handling layered responsibilities across jurisdictions, creditors, and coverage vendors. It also applies throughout refinancing, acquisitions, or portfolio restructuring, wherein smooth financial facts have an impact on both speed and consequence.

Conclusion

Escrow might seem insignificant, but at scale, it’s quite meaningful. Interest earned on trust balances is not a primary driver of returns. It is a signal. The capital is structured and predictable but underutilized.

For investors managing multiple LLCs, the real advantage lies in integration. When escrow is aligned with your broader financial system, it supports better liquidity planning, cleaner reporting, and more efficient operations. The hidden benefits are not in the rate itself. They are in active capital, structured flows, and an opportunity to reduce fragmentation across your portfolio.