What is a Journal Entry? Purpose, Types, Rules, Examples, and How to Record a Journal Entry?

In accounting, a journal entry is the foundation of recording financial transactions from day-to-day activities. As a business owner or beginner, you should know how to record an entry in journal.

Hence, to help my readers, I’ve compiled detailed information on journal entries, their importance, the recording process, three golden rules, a detailed example, and some common mistakes to avoid.

So, stay adherent to this article!

- What is a Journal Entry?

- What is the Purpose of the Journal Entry?

- What are the Different Types of Journal Entries?

- How to Record a Journal Entry?

- An Example of a Journal Entry

- How to Track Journal Entries?

- What are the Three Rules of Journal Entry?

- What are Common Journaling Mistakes?

- Wrapping Up!

- Frequently Asked Questions

Key Takeaways:

- Journal entries are recorded in chronological order.

- Total debits are equal to total credits in a business organization.

- In accrual basis accounting, transactions are recorded when they occur rather than when cash is exchanged.

What is a Journal Entry?

A journal entry is a record of every business transaction that is made in the company to reconcile accounts and transfer information.

It includes the date, accounts involved, and debit and credit amounts, along with a brief description of the transaction, maintaining accurate and verifiable accounting.

In accounting, most journal entries are made in chronological order and follow the double-entry bookkeeping method, meaning each transaction has a credit and a debit column. This signifies that journal entries are significant for recording relevant transactions to have a quick idea of the overall income and expenses. Whether you are managing complex transactions or looking to outsource your daily financial tasks, utilizing professional bookkeeping services ensures that every entry in your journal is accurate, compliant, and ready for tax season.”

What is the Purpose of the Journal Entry?

The sole purpose of the journal entry is to record business transactions in a chronological order, ensuring all monetary activities are physically and digitally documented.

It works as the backbone of accounting, providing a detailed audit trail for verification, and is posted to ledger accounts, income statements, and balance sheets.

Not only this, but accurate accounting entries are also essential for the auditing process. It reduces errors and allows for necessary adjustments to ensure compliance with standards like GAAP and IFRS. Interestingly, it is the foundation for businesses to monitor cash flow, expenses, and overall financial health.

What are the Different Types of Journal Entries?

There are 8 types of journal entries, such as recurring, nonstandard, accruals and deferrals, adjusting, reclassifying, closing, consolidating, and proposed audit adjustments. If you find yourself struggling with these specific areas, many businesses rely on dedicated payroll accounting services or professional year-end accounts services to ensure these critical journal entries are handled correctly.”

Here are the following types of journal entries in great detail.

1. Recurring Journal Entries

Recurring journal entries are repetitive transactions that are automated with the company’s accounting software.

For example, the company has to pay three years’ rent, i.e., $2,000.

2. Nonstandard Journal Entries

Nonstandard journal entries are not repetitive, and they happen once or twice a year.

For example, impairment charges, writing off bad debts, legal settlements, and stock buybacks.

3. Accruals and Deferrals

In the accrual basis of accounting, a company records revenues or expenses when earned or incurred, regardless of cash flow.

For example, a billing for March work is recorded in March and paid in April.

On the other hand, deferral accounting delays current cash flows into future periods. For example, prepaid expenses or rent/insurance paid in advance.

4. Adjusting Entries

Adjusting entries are documented at the end of an accounting period to record unrecognized income and expenses, ensuring financial statements follow the accrual basis.

For example, prepaid expenses, accrued expenses, accrued revenues, and depreciation.

5. Reclassifying Entries

Reclassifying entries moves amounts between different accounts to correct, adjust, or properly categorize financial statements.

For example, if a company records office expenses as miscellaneous expenses, adjusting entries help to move amounts. This entry has no impact on net income; it only reclassifies the amount.

6. Closing Entries

Closing entries are made at the end of the accounting period that transfer temporary accounts (revenues, expenses) to permanent accounts (equity).

For example, sales revenue is $10,000 in December 2025. It transfers to the permanent account and increases retained earnings. On 1st January, 2026, the sales revenue is again $0.

7. Consolidating Entries

Consolidating entries is used when two companies combine into a single set of financial accounts. It is used to eliminate intercompany transactions like sales, loans, or dividends between two entities.

For example, if company A is selling to company B, it is removed under consolidating entries to avoid double-counting.

8. Proposed Audit Adjustments

Proposed audit adjustments are corrections recommended by outside auditors to a company’s financial statements. These adjustments are related to unrecorded liabilities, classification errors, or revenue recognition.

For example, if an organization forgets to enter the accrued salaries of employees, an auditor must fix the incorrect capitalization of expenses.

Also Read: What is a CD Account? How Do CDs Work and How to Open Them?

How to Record a Journal Entry?

To record a journal entry, identify the transaction, recognize the affected accounts, determine debits and credits, write the transaction as a journal entry, and review and check. For founders and early-stage companies, leveraging accounting services for startups can save you hours of work each week and prevent costly accounting mistakes.”

Let’s take a look at the following steps for further guidance.

1. Identify the Transaction

Firstly, you need to identify the transaction or business event (cash received, paid expense, petty cash, etc.) when you are recording multiple transfers. It helps you create separate entries for each one.

For example, if you purchase a laptop for $1,200 with cash, this is a fixed asset purchase, which means that assets and expenses are involved.

2. Recognize the Affected Accounts

Secondly, you should determine which accounts are involved in the transactions to determine whether they increase or decrease. If accounting entries involve two or more accounts, you should make a note and mention each account.

For example, if a laptop is an asset purchased against cash, the accounts involved here will be fixed assets and cash.

3. Determine Debits and Credits

In accounting, “debit” refers to an increase in assets and expenses, and “credit” means an increase in liabilities and equity. Therefore, you should discover which type of transaction you are dealing with to record a journal entry.

For example, the fixed assets account is debited, and the cash account is credited in the journal entry.

4. Write the transaction as a Journal Entry

After gathering all the information, you can record a journal entry with specific accounts, accurate amounts, and credits and debits, along with a brief description.

For example,

| Date | Account | Debit | Credit |

| 12 January 2026 | Office equipment/Laptop | $1,200 | |

| To Cash A/C (Being a laptop purchased with cash) | $1,200 |

5. Review and Check

Ultimately, it’s important to review and cross-check all journal entries to ensure their accuracy and reliability. Once you are satisfied with the transactions, you can post them to other accounts, such as the general ledger.

For example,

Dr. Fixed assets A/C Cr.

| Date | Particulars | J.F | Amount | Date | Particulars | J.F | Amount |

| 12 Jan 2026 | To Cash A/C | $1,200 | |||||

| (Balancing figure) | $1,200 | ||||||

| Total | $1,200 | Total | $1,200 |

Dr. Cash A/C Cr.

| Date | Particulars | J.F | Amount | Date | Particulars | J.F | Amount |

| 12 Jan 2026 | By fixed asset A/C | $1,200 | |||||

| (Balancing figure) | $1,200 | ||||||

| Total | $1,200 | Total | $1,200 |

An Example of a Journal Entry

Here’s a detailed example of a journal entry with multiple transactions.

For example,

| Date | Transactions |

| January 26, 2026 | The owner invests $10,000 cash in the business for expansion. |

| February 1, 2026 | The expansion forces the company to purchase $1,500 of office supplies on account. |

| February 5, 2026 | The company also pays rent of $2,000 cash for January. |

| February 10, 2026 | $2,000 salaries are paid through bank transfers. |

Now, take a look at the journal entries of these transactions.

1. The owner invests $10,000 cash in the business.

| Date | Account | Debit | Credit |

| January 26, 2026 | Cash A/C | $10,000 | |

| To Capital (The owner invested cash in the business.) | $10,000 |

2. The company purchases $1,500 of office supplies on account.

| Date | Account | Debit | Credit |

| February 1, 2026 | Supplies | $1,500 | |

| To Accounts Payable A/C (Being office supplies purchased on account) | $1,500 |

3. The company paid $2,000 cash for rent.

| Date | Account | Debit | Credit |

| February 5, 2026 | Rent A/C | $2,000 | |

| To Cash A/C (The rent being paid for January) | $2,000 |

4. The company paid salaries of $2,000.

| Date | Account | Debit | Credit |

| February 10, 2026 | Salaries A/C | $2,000 | |

| To Bank A/C (Being salary-paid) | $2,000 |

How to Track Journal Entries?

Tracking your journal entries is essential for maintaining the financial integrity of businesses. Similar to checking your personal bank statements, it ensures that all financial transactions are accurate and recorded in specific accounts.

To track your accounting entries, you should follow these best practices.

- Establish a standardized procedure for recording journal entries.

- Invest in modern accounting software.

- Record in chronological order.

- Always check that entries include all necessary transactions and information.

- Reconcile your books regularly.

- Implement strict data security to prevent unauthorized access.

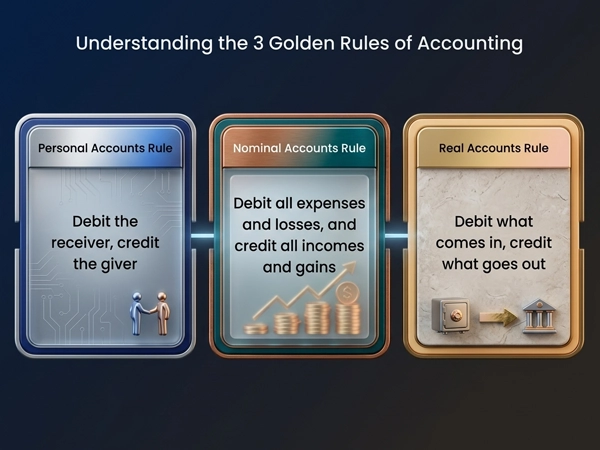

What are the Three Rules of Journal Entry?

The three rules of journal entry in accounting are related to debit and credit information. Let’s skim through this section to acknowledge these rules in great detail.

Rule 1: Debit the Receiver and Credit the Giver (Personal Accounts)

It means that you should debit the account of the person who receives money and credit the account of the person who gives value.

Rule 2: Debit What Comes in and Credit What Goes Out (Real Accounts)

This highlights that increasing an asset account (e.g., buying machinery) is a debit entry, and decreasing an asset account (e.g., selling furniture) is a credit entry.

Rule 3: Debit Expenses/Losses and Credit Income/Gains (Nominal Accounts)

It means that all expenses and losses are recorded in the debit column and all income and gains are recorded in the credit column.

What are Common Journaling Mistakes?

There are common journaling mistakes beginners can make, including inputting incorrect amounts, unbalanced amounts, recording under the wrong accounts, formatting inconsistencies, and a lack of order.

Here are the following mistakes, thoroughly.

- Inputting Incorrect Amounts

Always make sure that you put accurate amounts in your journal entry for making the right ledger account, especially when you input data manually.

- Unbalanced Amounts

When you opt for double-entry accounting, each transaction must balance with equal debits and credits. The unbalanced amounts show the errors and misstatements in journal entries.

- Recording Under the Wrong Accounts

Cross-check that transactions are recorded under the correct accounts. For example, if the company paid salaries, it will be mentioned in the salary account.

- Formatting Inconsistencies

Use the same format to record transactions in the journal entry, including date, accounts, debit (left side), and credit (right side). It helps you to maintain the proper financial records.

- Lack of Order

In double-entry bookkeeping, journal entries are recorded in chronological order. It means recording business transactions, events, and data systematically as they occur.

Also Read: How are Dividends Taxed? A Beginner’s Guide to Smart Investing

Wrapping Up!

To sum up, a journal entry is the backbone of a business. It is important to record day-to-day activities for running financial accounts, and journal entries help you to maintain them.

Moreover, you also assess business success and make informed decisions to grow your revenue value. If you find it difficult to record accounting entries, you should contact an accounting professional or invest in automated software.

Frequently Asked Questions

Ans: A journal entry is a business transaction record in accounting with a professional format, including date, accounts, debits, credits, and a brief description.

Ans: The 4 parts of a journal entry are the following:

- Date of the transaction

- Affected accounts

- Debits and credits

- Brief description of the transaction

Ans: The two types of journal entries are the following:

- Simple Journal Entries: Records a straightforward transaction that affects only two accounts.

- Compound Journal Entries: Includes complex transactions that affect multiple accounts.

Ans: The three golden rules of journal entry are:

- Debit all expenses and losses, credit all income and gains

- Debit the receiver, credit the giver

- Debit what comes in, credit what goes out

Sources: