Cash Flow Statement: See How to Calculate It and Draft One With Examples

In financial accounting, a cash flow statement plays a vital role in assessing the financial health of a business. It provides the monetary valuation of actual cash income and expenditure within a business and shows how money enters and leaves the organization.

Every business, whether large or small, needs to keep track of its statement of financial flows in order to monitor its growth and net loss. Yes, the financial flow statement can prevent your company from being bankrupt.

Intrigued!?

Hop into this article to learn about cash flow statements, as I have comprehensively discussed financial flow statement basics with financial statement examples for an easy understanding.

- What is a Cash Flow Statement?

- Why is the Cash Flow Statement Important?

- Components of the Cash Flow Statement

- How to Calculate a Cash Flow Statement? Direct vs. Indirect Method

- How to Prepare a Cash Flow Statement?

- Difference Between Cash Flow Statement and Balance Sheet

- How Does Income Tax Impact the Cash Flow Statement?

- Cash Flow Financial Statement Example

- Summing Up!

- Frequently Asked Questions

What is a Cash Flow Statement?

A cash flow statement is one of the three key elements of financial accounting. The statement of cash flow represents how capital or cash equivalents’ inflow and outflow in the company during an accounting period.

The purpose of this statement is to provide a detailed financial status of a business, along with an income statement and balance sheet. Moreover, it provides deep insights to examine the overall growth of a company.

Whether you’re a business owner, investor, or working professional, a statement of financial flow helps you analyze how cash moves in and out of the business.

Why is the Cash Flow Statement Important?

As you’ve been informed, cash flow statements show the working capital and expenses of a company. It helps to evaluate the financial health of a business, which ultimately results in better operations for maintaining the growth of an organization. Simply put, it is an essential part of a financial analysis of any venture.

Here are a few reasons why your company needs a financial flow statement.

1. Insights into Spending Operations

By preparing cash flow statements, you, as an entrepreneur, can easily monitor the company’s expenses. It gives an all-inclusive picture of payments that aren’t typically recorded in a Profit and Loss account.

For Instance: If your business takes out a loan and pays interest back-to-back, it wouldn’t be mentioned in the Profit and Loss statement. Instead, it will be recorded in statements of financial flow, as it clarifies the real-time overview of the cash outflows of a company.

2. Liquidity Analysis

Liquidity is a company’s ability to convert assets into cash to cover debts, expenses, and reinvestment. It helps you know what you can afford and what you can’t. Unlike the income statement, which shows profits on paper, the financial flow statement focuses on actual cash available in bank accounts.

For instance: A business’s net profit is $15,000 in an income statement, but a cash flow statement only shows the current cash of $5,000. It represents the actual cash of a company instead of the overall profit. Hence, this could assist you in analyzing cash availability to avoid a shortage of money.

3. Maintaining Short-Term Planning

Moreover, a detailed financial flow statement helps to achieve short-term goals efficiently as it focuses on recording how much real cash a company has in hand at a specific time. It can assist a financial advisor in keeping track of spending activities and analyzing cash flow in the future.

For instance, A retail store owner checks its cash flow statement to monitor cash inflow (sales) and outflow (rent, wages) for the next few months. This helps him to track the financial condition of his shop for future planning and adjustments.

Hence, preparing a statement of financial flow prevents the business from bankruptcy and meets daily commitments.

4. Review Working Capital

Working capital is defined as the funds that are currently available in the business, such as the amount of cash, deposits, and other finance sources. The cash flow statement maintains the record of working capital for a business in order to analyze cash outflows and inflows. It is useful in managing operations and day-to-day expenses.

For instance:

Calculate the working capital of a XYZ company.

Current Assets – $130,000

Current Liabilities – $80,000

If you want to compute the working capital of your business, you must subtract all liabilities from your current assets. The outcome is your actual working capital or cash, which you can use to operate tasks in your firm.

Working Capital = Current Assets – Current Liabilities

$130,000 – $80,000 = $50,000 (positive)

This means that XYZ company has enough assets to cover its financial expenses and debt. The cash flow statement is important to monitor such cash flows to avoid financial issues in a firm.

5. Crisis Management

It is clear that a statement of financial flow represents a detailed report of cash flows in a company. It assists business stakeholders in analyzing whether they have excessive cash or a cash shortfall. This helps in managing crises by adjusting to challenges over the period. It provides a potential summary that could make an enormous difference for the company’s growth.

For instance: By analyzing a cash flow statement’s negative result, a company can cut off expenses to cover urgent liabilities. It will help the business owner protect his venture from bankruptcy and stabilize its finances for the short term.

Also Read: Master Cost Accounting: Its Functions, Formulas, and Limitations

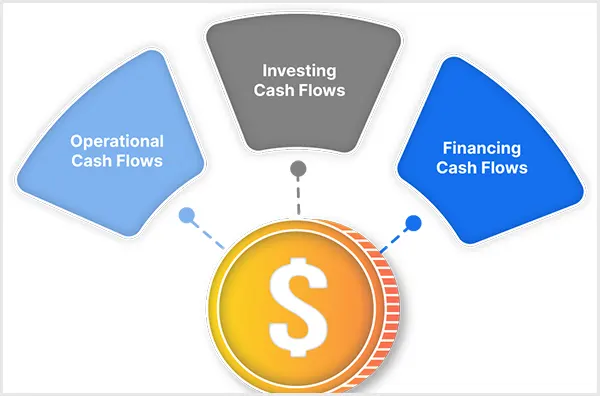

Components of the Cash Flow Statement

Generally, there are three components of financial flow statements: operating, investing, and financing. Professional bookkeepers, accountants, and financial advisors rely on these principles to prepare relevant statements.

Here is the breakdown of the three components:

1. Operating Activities

Operating activities show how cash inflows and outflows from a company’s core business operations. It records all the activities that aim to bring money into a business, excluding investment.

A positive operating cash flow denotes enough cash in an organization to cover expenses. However, a negative cash flow may be an alert for a deficit in working capital.

For example, if you own a pizza restaurant, cash flow from operating activities records the cash you spend on ingredients/services and the cash you earn by selling pizzas.

Cash inflows from operating activities include:

- Interest received on loans

- Receipts from the sale of goods and services

- Dividend income

- Cash received from other business organizations

Cash outflows from operating activities include:

- Payments to suppliers

- Salaries and wages

- Rent and income tax payments

- Other payments for operating expenses

2. Investing Activities

The investing section covers long-term investments, which are responsible for the company’s future success. It includes the purchase and sale of land, plants, and cash equivalents. When the cash is spent on an investment, it makes an asset of the same value.

Consequently, if assets are frequently sold to generate cash, it might lead to financial distress. Not only this, but extreme spending without operating cash flow can also strain liquidity.

For example, if you spend $10,000 to purchase land for your company, you lose $10,000 in cash. So, in the cash flow statement, cash on hand ($10,000) is deducted in purchasing an asset.

Cash inflows from investing activities include:

- Selling assets

- Cash receipts from interest

- Dividends received as returns on loans

- Debt instruments of other agencies

- Equity securities

Cash outflows from investing activities include:

- Cash payments for loans

- Payments into investment pools

- Payout to acquire equity instruments

3. Financing Activities

In financing activities, the statement specifies the net amount of funding that a company generates during a specific period. It shows how an organization raises funds and repays debts/equity in business operations and expansion.

However, raising debt without strong revenue growth poses risks. Besides this, consistent dividends and stock buybacks increase financial liquidity, which strengthens the shareholder value of the company.

For example, you received a loan of $50,000 from a bank for a year. So, it should be recorded as a $50,000 increase to cash on hand because your bank balance rises.

Cash inflows from financing activities include:

- Issuance of equity and debt

- Borrowing from financial authorities

- Spending cash to repurchase shares

- Government grants

Cash outflows from financing activities include:

- Dividend payments

- Payment of interest on debts

- Redemption of convertible securities

- Repurchase of Equity

How to Calculate a Cash Flow Statement? Direct vs. Indirect Method

Now that you understand the importance of the cash flow statement and its three major components, you’re all set to learn how it is calculated. Here, in this section, I will help you to create a relevant statement of cash flow for your business.

There are two ways to calculate the financial flow statement: one is direct, and the other is the indirect method. Below, I’ve described both approaches in great detail.

Cash Flow Statement Direct Method

Using the direct method, you can record actual cash inflows and outflows from operating activities directly. To calculate transactions of the operating section, you can add all cash received in the statement and subtract all cash payments.

Moreover, it requires tracking of every cash in and out, which takes time to prepare a statement. This method may be challenging for businesses due to multiple transactions.

For example:

Using the direct method.

| Add: Cash Receipts | |

| Cash collected from customers | $500 |

| Loan received | $700 |

| Interest income | $100 |

| Income tax refund | $50 |

| Total Cash Inflow (Sum) | $13,500 |

| Less: Cash Payments | |

| Direct service costs | $350 |

| Salaries | $500 |

| Payment to suppliers | $150 |

| Total Cash Outflow (Sum) | $1,000 |

| Net Cash (Positive) | $12,500 |

This cash flow statement example indicates that the company has enough cash inflow for business expansion and future payments.

Cash Flow Statement Indirect Method

In the indirect method, you can start with net income and adjust for non-cash items like depreciation and cash-based transactions. Unlike the direct method, it depends on accrual accounting (records revenues and expenses when they are earned or incurred). The net income will convert into actual cash by removing the non-cash payments from the income statement.

Comparatively, it is a simpler and faster method to prepare a cash flow statement for larger businesses than the direct method.

For example:

Using the indirect method.

| Net income | $10,000 | |

| Add back depreciation | $20,000 | |

| Adjusted Net Income | $30,000 | |

| Cash from Operating Activities | ||

| Increase in accounts receivable | ($5,000) | |

| Interest received on loans | $100 | |

| Total Cash from operating activities | $25,100 | |

| Cash from Investing Activities | ||

| Sale of machinery | $10,000 | |

| Purchase of computers | ($2,000) | |

| Total Cash from investing activities | $8,000 | |

| Cash from Financing Activities | ||

| Bank loan | $50,000 | |

| Payment to line of credit | ($15,000) | |

| Total Cash from investing activities | $35,000 | |

| Total Cash generated for the year | $68,100 | |

| Add cash at the beginning of the year | $20,000 | |

| Cash at the end of the year | $88,100 |

How to Prepare a Cash Flow Statement?

After carefully analyzing the methods and financial statement examples, it’s time to learn how to create a cash flow statement. In this section, I’ve exclusively mentioned the steps that one should follow for preparing an error-free financial flow statement.

Well, at first glance, preparing any such money flow sheet might look a bit challenging. But as you progress through every day, it becomes a piece of cake.

Here, I’ve jotted down essential pointers that will be helpful for you to prepare a statement.

1. Estimate Staring Balance of the Year

Primarily, determine the starting balance of cash and cash equivalents to prepare a cash flow statement. You can easily find the transactions from the income statement of the same year.

Notably, cash at the beginning of the year is essential for the indirect method. However, it is not calculated in the direct method.

2. Calculate Cash Flow from Operating Activities

Once you have your starting balance, calculate all cash transactions, whether outflow or inflow. It helps you to determine how much of your organization’s finances come from cash.

Either use the direct or indirect method; both have the same number of outcomes, except for the process of calculations. Plus, both methods are accepted by Generally Accepted Accounting Principles (GAAP) and the International Financial Reporting System (IFRS).

H3: 3. Evaluate Cash Flow from Investing Activities

After operating activities, you need to calculate transactions from investing activities. This section includes cash flows related to buying and selling assets like property and equipment.

Besides this, you have to keep in mind that investing activities only include cash flows with actual cash, not debt.

4. Compute Cash Flow from Financing Activities

This last section involves both debt and equity to examine cash flows from financing activities. It includes settlement from raising cash and payments to debt. However, you have to decide between different calculations while using GAAP and IFRS.

Firstly, the dividends paid are recorded in financing when using GAAP and maintained in operating activities according to IFRS. On the contrary, interest paid is included in finance under IFRS; otherwise, it is used in operation when using GAAP.

5. Sum Up the Ending Balance

When you calculate all cash flows from operating, investing, and financing activities, you have to determine the ending balance. The ending report for the year indicates the financial condition of the company.

A positive cash flow means that the firm earns more than it spends. Conversely, a negative cash flow reveals that it spends more than its earnings.

In simple terms, you have to consider all transactions from three main components to prepare an appropriate cash flow statement. It helps you to take significant steps for your business development.

Suggested Read: What is Retro Pay? Meaning, Examples, and How it Works

Difference Between Cash Flow Statement and Balance Sheet

Along with the statement of financial flow, the balance sheet is an essential component of financial accounting. Many beginners are always confused between the roles of the balance sheet and the statement of cash flow.

That’s why I’ve prepared a detailed breakdown of the Cash Flow Statement and Balance Sheet.

| Basis | Cash Flow Statement | Balance Sheet |

| Purpose | It represents cash inflows and outflows during a particular period. | Used to show the financial status of a company at a specific point in time. |

| Focus | Basically, it focuses on the cash transactions for the year. | Emphasizes the economic situation of a firm by comparing performance over time. |

| Components | Operating, Investing, and Financing activities. | Assets, Liabilities, and Equity of Stakeholders. |

| Accounting Parameter | Records only cash-based transactions. | Record both cash and non-cash transactions. |

| Usage | Measure the ability of the firm to generate cash and its management. | Measure the financial liquidity and stability of the firm. |

| Limitations | Does not show a detailed report of the financial status of the organization. | Does not provide significant information on cash flows. |

How Does Income Tax Impact the Cash Flow Statement?

Proper tax planning is indispensable for a company’s growth. If you have a long-term income tax as a liability, it can affect your business’s economic circumstances in the future. So, you need to maintain income tax and other direct and indirect taxes in the financial statements.

Firstly, income tax payable on your current profits is recorded as a liability in the balance sheet. Then, the tax incurred as an expense of a present period is maintained under the income statement. After that, the cash flow statement reports the actual tax paid as a cash outflow in the quarter, month, or year.

Generally, operating activities include income tax paid from the statement. In the indirect method, it is written in the statement at the beginning or in the footnotes.

Thus, the report of income tax payments in the statement is crucial. It provides insights to stakeholders and financial advisors to understand the company’s position and stability.

Cash Flow Financial Statement Example

Let’s understand how to record entries with a detailed example for a better understanding.

Example: Calculate the ABC Fashion Pvt. Ltd. accounting entries to prepare a cash flow statement using the indirect method.

| Cash Flow Statement | ||

| ABC Fashion Pvt. Ltd. | ||

| Net Earnings | $50,000 | |

| Cash Flow from Operations | ||

| Depreciation | $10,000 | |

| Increase in tax payable | $5,000 | |

| Decrease in Accounts receivable | $20,000 | |

| Salaries paid | $35,000 | |

| Payments to suppliers | $10,000 | |

| Total cash flow from operations | $40,000 | |

| Cash Flow from Investing | ||

| Sale of machinery | $65,000 | |

| Cash receipts from interests | $5,000 | |

| Dividends received as return on loan | $22,000 | |

| Purchase of printers | $15,000 | |

| Purchase of equipment | $30,000 | |

| Total cash flow from investing | $47,000 | |

| Cash Flow from Financing | ||

| Notes payable | $20,000 | |

| Government grants | $5,000 | |

| Total cash flow from financing | $25,000 | |

| Total cash generated | $112,000 | |

| Starting Balance of the year | $42,000 | |

| Cash at the end of the year | $154,000 | |

Summing Up!

Cash flow statements are the most important financial document of the company. By preparing and analyzing the statement of cash flow, you can easily understand the firm’s financial health.

Additionally, it demonstrates the firm’s ability to raise finances and manage the crisis through business operations. This statement provides a detailed insight to investors and entrepreneurs about the organization’s stability.

If you also own a business, whether small or large, creating a cash flow statement should definitely be on your checklist.

Read Next: Corporate Accounting: Definition, Importance, Types, and Career Potential in 2025

Frequently Asked Questions

Ans: There are three components of cash flow statements:

- Operating Activities

- Investing Activities

- Financing Activities

Ans: One can easily calculate a statement of cash flow with two different methods:

- Direct Method

- Indirect Method

Ans: Depreciation for tangible assets (buildings and equipment) and amortization for intangible assets (copyrights and patents) are added back to net income in the cash flow statement.

Ans: You can use a cash flow statement to analyze how much cash you have to cover the expenses of your business. It will prevent your business from going bankrupt and help you meet daily financial tasks.

Sources: